It’s summer break, and school is officially out for the kids! If you’re a parent like me, you’re probably already counting down the days until your child goes back to school. While the dirty floors, dishes in the sink and laundry can wait; there is one thing that you should not wait on. What do I speak of, you may be asking? I am talking about something no parent wants to talk about, but that every parent needs, an insurance policy for your child. Why would a child need an insurance policy?

The thought of having a sick child, or losing a child, is something that no parent should ever have to go through. However, you can take an insurance policy on your children, so if the worst should happen, there is coverage in place to aid your family.  The benefits of placing your child with an insurance policy are:

Ensure your children are protected by contacting our company for a free, no-obligation quote! To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.

0 Comments

I read an article recently, which has prompted me to write this post and with June being Pride month; this article could not come at a better time. According to the report, which is cited at the bottom of this blog, Iowa State University's Ivy College of Business found approval rates for same-sex couples were between 3% and 8% lower than for heterosexual couples. I realize this study is based out of the United States, and I like to think that as Canadians, we are little further ahead with acceptance compared to our southern neighbors. However, we have had clients from the LGBTQ+ community who have told us they have been afraid of applying for insurance for fear that they will be turned down for who they are or who they love. Let me make one thing perfectly clear before I go any further. Regardless of who you identify as or who you choose to love, there is something that you cannot forgo; and that is insurance. Rest assured that at Broker Plus Insurance, we do not impose a rating, nor discriminate clients based on their sexual orientation or gender identity. In fact, sexual orientation is not even asked on any of our applications because that’s your business, not ours! We offer several different products for clients from all walks of life to ensure that their needs are covered with the best product possible. We have Term options of 10, 20 and 30-years; three No Medical products for clients with previous health conditions and specialty products such as Critical Illness and a Job Loss Rider to our Mortgage Disability insurance. We even have child riders for Critical Illness and Child Protection that can be added to our Term life insurance, which covers biological children AND adopted children.  Regardless of who you love or who you are, we should all share the same love for insurance. Contact our office today to find out how you can protect yourself and your family.

To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. **Source https://www.mortgagebrokernews.ca/market-update/do-mortgage-lenders-discriminate-against-samesex-couples-256558.aspx?utm_source=Pinpointe&utm_medium=20190418&utm_campaign=MBN-Morning&utm_content=CD515713-56DD-42B4-A34A-AC106012B56D&tu=CD515713-56DD-42B4-A34A-AC106012B56D   There have been many clients who have contacted us recently wanting to gain a quote for Term insurance. As our clients become savvier in their purchase, they want to compare mortgage insurance with term insurance. The main selling feature of a personal policy is that the coverage does not decrease, and the client is the policy owner, but did you know that not all term policies are the same?

10-year term policies are often the first personal product that is offered to clients. While it may look cheaper than mortgage insurance, the rates jump up considerably every 10 years. With some policies these rates aren’t even locked in, so you won’t know your renewal rate until it’s time to renew! A typical mortgage will go for 25-30 years so you will need a policy that is affordable the whole way through! We find many clients are surprised to know that we carry Term products that allow coverage of 20 and 30 and even 100 years because often, their mortgage broker will only offer 10-year terms if that. What is the benefit of choosing a longer term?

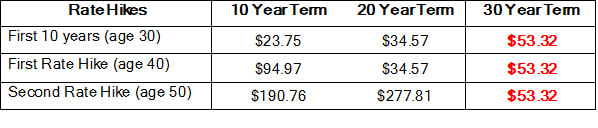

As you can see from the chart below, the rates for a 20 or 30-year Term are much better for your needs in the long-term. The premiums below are based on that of a 30-year-old male non-smoker for $500,000 who’s mortgage will be paid off in 25 years. While at first glance it may seem cheaper to take a 10-year term; keep in mind that with a 20 or 30-year term you are paying the same rate for those 20 or 30 years which makes a 30-year term more cost affordable in the long run! When your term comes up for renewal, they always have the option of renewing at a lower term or amount depending on when they will have their mortgage paid off. Our friendly staff will help you navigate the different insurance options out there and make sure you make the best decision for your family! To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  For some people, the concept of insurance can seem like a losing battle at times. The process of obtaining insurance can create anxiety for those with certain lifestyle habits, potential health concerns or for those who may have been declined for insurance in the past. While insurance is no doubt scary for these individuals, it shouldn’t be an excuse for them to forgo it simply because they think they won’t qualify. We have access to a few carriers who have created insurance products for this group of people to ensure their needs are being met. #1 – No Medical Life:

There’s no excuse for you to settle for an Accidental Death policy as we have full policies that can cover them; should you have a history of medical conditions many other companies may not place a policy with. Make sure that you and your family have all your insurance needs covered, without sacrificing the integrity of their insurance policy. Contact us today for more information!

To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  We’ve heard almost every excuse in the book from our clients regarding why they think insurance is not an urgent matter. While aspects such as budget, sudden vehicle work, or a rainy day can lead one to tighten the grip on their wallets; there is never a “good” excuse not to have insurance. The alarming fact is that if you are living with a tight budget, you are actually in need of insurance the most. Consider what would happen if you were suddenly disabled and unable to work for eight months, or worse, you or your spouse pass away unexpectedly. Do you have one year’s living expenses tucked away to see you through months of reduced income or the loss of an entire income?

1. I have life and disability coverage through work. This is a common rebuttal we hear almost every week and while health and extended benefits through work are a fantastic thing to have; they are usually not enough to cover you if something were to happen. As an example, my husband makes $60,000 per year, and his work coverage pays three times his yearly salary if he dies; which equates to $180,000. While this may seem like a decent amount; when you factor in costs such as childcare, mortgage payment, living expenses, vehicle insurance and maintenance, food, clothing, and other necessities; it’s easy to see that this amount will not be sufficient to sustain my family’s long-term needs. The other major concern is what happens to his coverage if he loses his job? It is always smart to have a personal policy that belongs to YOU and not your employer. 2. I have a history of health conditions; no company will cover me! Broker Plus Insurance is proud to offer three No Medical products in Life, Disability and Critical Illness for those who may have a history of past health conditions or who do not want a medical exam as an underwriting requirement. The benefit of these products is that they provide three different insurance options for those who may be turned down or have been turned down in the past. The best thing about this product is that there are three different rating structures for clients interested in this product; thus almost every client can be covered under this policy. If, for whatever reason, your client cannot be covered under this type of policy; even having an accidental death only policy is better than no coverage at all! 3. We’re living paycheque to paycheque; we don’t have enough money for an insurance premium. This is by far the most common rebuttals we hear from clients, and we understand that with a new mortgage, utility bills and a family to feed; there isn’t much money left for anything else at the end of a paycheque. However, there are several “necessities” that we spend money on which can be cut back or put towards insurance. A typical example is those who stop off to get coffee every morning. Let’s assume it’s just a coffee and the going rate for that is $2.50 – what if I told you that insurance policies could cost as little as $1 to $2 per day? It’s true, and something that could easily be cut back to have coverage in place. Another option is to do partial coverage so that there is at least some coverage in place, should something happen. Contact us today for more information about how we can take care of your families insurance needs. To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  We get asked this a lot by clients when going over the different coverage options they can take. In the scheme of ranking insurance products by importance, we tell clients that’s a personal decision but one that they should look at closely. While being optimistic about one’s future health is by no means a bad thing, it is essential to be realistic and here are some cold, hard facts about just how widespread critical illnesses are today.

Unlike disability coverage, folks often associate critical illnesses will older generations. That’s just simply not the case. More and more homeowners between the ages of 40 and 60 are suffering a critical illness. Unfortunately, the recovery from one of them can have more impact than recovering from a short-term disability. We have access to several critical illness products that cover up to 25 different illnesses from a $50,000 payout to a million. The lump sum benefit from these policies can be used for anything the insured chooses to use it for from income replacement and rehabilitation to a celebratory vacation once recovered. What your clients want to spend this money on is entirely up to you. Broker Plus Insurance is proud to offer a wide range of critical illness products to ensure your needs are met. These products include: Standalone Critical Illness insurance (both 10-year renewable and level to age 75) Critical Illness Rider for our Term insurance Critical Illness Rider for children Standalone Critical Illness for children No Medical Critical Illness for those who may be hard to insure. Don’t let this critical product slip through your grasps contact us today for more information! To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. *Statistics are from the Heart and Stroke Foundation of Canada.  With the New Year upon us, many of us are making resolutions that hopefully, we will try to keep going throughout the year. While many people are opting for one-month resolutions such as the January 31 day yoga challenger or dry January, for those who may have overindulged during the holidays, there are others who want to keep a resolution for the whole year. However, there is one resolution that you should follow; putting your family’s insurance needs first.

While you may be intrigued by what your advisor at the bank says or what your friend said worked for them, they may not have your best interest in mind. For example, many banks do not offer products for clients who may be harder to insure, and as a result, these clients will only be placed with an Accidental Death policy which is not in the client’s best interest. Alternatively, how about if you are looking for personal coverage or job loss or critical illness that they may not have access to? The answer – contact Broker Plus Insurance for a FREE no-obligation quote! Why Choose Broker Plus Insurance?

To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  In the words of Bob Dylan, “the times are a changing.” With marijuana now legalized in Canada, the smoke is starting to clear regarding how companies are rating those who smoke marijuana. Many companies have already made adjustments to their policies for those who consume marijuana, specifically, about smoker rates. For certain companies, those who consume under a certain amount of marijuana per week can now qualify for non-smoker rates!

Broker Plus Insurance is proud to offer mortgage insurance and term life products through Great-West Life and Western Life who both allow marijuana users to be eligible for non-tobacco status on an individual case by case basis provided that there has been no other use of tobacco products, nicotine or e-cigarettes in the previous 12 months. This new amendment is excellent news for those clients who may not have taken insurance because they “smoke a little bit of weed” occasionally or who may have turned down insurance in the past as they were afraid they would not qualify or did not want a rated policy. Another one of our providers, Canada Protection Plan, enables clients who smoke marijuana up to four times a week to qualify for non-smoker rates! This policy is perfect for clients who are regular users of marijuana as it is very generous in the amount they are allowed to light up. These clients are eligible for:

Insurance is something that everyone needs dude! Contact us today to for more information! To request a quote on the products we offer, click here. Alternatively, call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  Image from Getty Images With Halloween happening at the end of this month, there is no doubt that many of you may be partaking in the festivities by watching horror movies, eating copious amounts of candy and taking your children out trick or treating. With all the ghost, goblins and witches that will be on our streets over the next few weeks, I felt compelled to write a post about something potentially horrifying – not having insurance. According to a study conducted by the investment firm Edward Jones, less than one-third of Canadians have insurance coverage for serious life events. The study goes on to say that 23% of Canadians answered that they are not financially prepared if they pass away too soon and only16% said that they had purchased life insurance that would cover their remaining mortgage payments should they ever pass away.*

With this information, the sheer thought of not having any insurance in place is enough to frighten Jason Voorhees himself. Luckily, there is a solution, and that solution is simple – buy insurance. Now here’s the tricky part, not everyone likes the concept of insurance. At Broker Plus, we try to keep insurance simple, affordable and stress-free by educating you about the benefits of the products while forgoing the jargon that can leave clients scratching their heads. However, we’ve noticed a trend with clients who still feel overwhelmed when they get insurance quotes because, let’s face it, thinking about one’s mortality or morbidity is usually not a happy topic to discuss. Here are some ways you can navigate through the fog when it comes to insurance: 1. A Quiet Place – find a quiet place that brings some peace to you. Take 5-10 deep breaths before you begin reviewing your options, this will help you think more clearly as opposed to being “stressed” about the thought of your morbidity and mortality. It may be best to get out of the house and find a nice, quiet place (assuming your home has a screaming 20-month-old as mine does) to be able to become fully focused on what your true needs are. 2. The Others – often children get forgotten about when homeowners take out insurance policies when ideally it is the best time to add a child rider to a policy for products such as Term Life. The riders are usually affordable, $10 per month for $20,000 amount of coverage, which is cheaper than two specialty coffees at Starbucks. 3. Let The Right One In – if you’re getting multiple quotes from different companies it can sometimes be hard to make clear decisions without feeling overwhelmed. Broker Plus Insurance has been working with Canadians for over 20 years with our focus on helping mortgage clients be more aware of the different options that are available to you. We also can do partial coverage for folks who are worried about the premium amount or who have additional coverage already in place. 4. As Above, So Below – what if I told you that for those 3 points above Broker Plus Insurance could do all of those things for you? No, it’s not a trick, at Broker Plus Insurance we put your needs first and have a full-service center open five days a week to assist you with any questions you may have. We can even do evening and weekend calls! We do the shopping around for you, so you can rest assured that we have your best interest in mind and try our best to provide you with the cheapest premium while not sacrificing the quality of the coverage offered. With a full-service center that genuinely cares about its clients and puts their needs first, does insurance seem that scary? Contact Broker Plus Insurance today for a no-obligation quote to ensure that you and your families insurance needs are being met! To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. *Sources cited from https://www.insurancebusinessmag.com/ca/news/breaking-news/most-canadians-are-underinsured-study-62245.aspx  One question we get asked a lot at Broker Plus Insurance is about how Term insurance differs from traditional Mortgage insurance. A lot of times, clients can get overwhelmed when they are taking out a mortgage, especially if it is their first mortgage. They may feel rushed into making a decision or decide not to take any coverage which results in them not making a sound decision about which coverage is best for their family and themselves or not having any coverage when something horrible happens. With a lot of “fake news” out there, we wanted to try to clear a few things up about some of the common misconceptions surrounding term insurance.  Misconception #1 – Term insurance is not portable:

The main benefit of Term insurance is that it is portable from lender to lender, property to property, unlike traditional Mortgage insurance. All of the policies we offer at Broker Plus Insurance are fully portable (and sometimes convertible) you can rest assured that if they move or if your needs change you can be confident that your insurance will have some flexibility as opposed to if you had taken insurance through the bank. Misconception #2 – You can’t choose your beneficiary: Another massive benefit of Term insurance is that the life insured can select their beneficiary who will receive the value of their policy if they die. While traditional Mortgage insurance will pay the lender so that the mortgage is paid off the benefit of Term insurance is that the funds could be used for things other than the mortgage such as childcare costs, funeral expenses and whatever else your beneficiary chooses to do with the money. Misconception #3 – Term insurance declines as the mortgage is paid off: Term insurance DOES NOT decline in amount unlike Mortgage insurance; if you want $500,000 coverage, they will have that $500,000 for the entire time the policy is in place. If you had $300,000 owing on their mortgage when they passed away their beneficiary would still receive $200,000 assuming they used $300,000 to pay off the remaining mortgage. Misconception #4 – Term insurance is only for short term: At Broker Plus Insurance, we are proud to offer Terms of 10, 20, 30 and even 100 years! Locking in for the most extended term your budget will allow is always a smart move. While 10-year term premiums look attractive up front, the new higher premium every 10 years is NOT. We will explain the ins and outs of term insurance to you so that you can compare it with mortgage insurance and make the best decision! Don’t be led astray by “fake news” contact Broker Plus Insurance today! We promise to make your insurance needs come true, on your terms. To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. |

Author

All blog posts are written from Cassie Meadows, a Broker Account Manager at Broker Plus Insurance.

Archives

March 2021

Categories

All

|

RSS Feed

RSS Feed

|

|

|

|