Over the last two months, we’ve seen an increase in clients requesting insurance through our company due to the COVID-19 outbreak, even those who had previously turned it down. When it comes to a person’s health and safety, it’s a natural response to want to know you have all your bases covered should the unthinkable happen. The great thing about Term insurance is that it can be put on at any time. When we tell clients about the benefits of this type of coverage, we find that we catch them off-guard because there’s a lot of misconceptions about the benefits of Term insurance over mortgage insurance. Being able to break down these misconceptions and benefits is one of the best parts about utilizing Broker Plus Insurance for your insurance needs, as our Life Agents can go over these aspects with you in depth.  The Benefits of Term Insurance Are:

With what’s been happening in our country with COVID-19, having insurance in place has never been more important. Protect yourself, protect your family, and contact us today for more information. To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.

0 Comments

We’ve been hearing a lot of concerns from our clients about obtaining insurance during this time of uncertainty in our society due to COVID-19. Many clients think that applying for insurance is something that requires to be done in-person, which isn’t the case with any of the carriers used here at Broker Plus Insurance! We can take applications over the phone, and paperwork can be signed and scanned or faxed back to us for processing.

How Do We Make This Work?

Yes, it really is that easy to apply for insurance while respecting social distancing. We have access to a wide range of products to ensure that your entire family is covered! To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. The fear of claims not paying out is a fear that leads many people to be wary about insurance and, in some cases, not to take insurance at all. In my opinion, there is no higher gamble than to gamble with one's life. When one's life is not insured, it is a gamble that will almost always end in a loss for more than one person. While it is unfortunate when we hear that a claim doesn't payout from one of our clients, it is imperative to note the reasons why claims will out payout. By analyzing the common misconceptions about the life insurance industry, it will allow you to understand why some claims cannot be paid out.  #1 - You Were Dishonest On Your Application: We like to believe that every client we speak to is telling us the truth, however; sometimes, this is not the case. In cases of fraudulent misrepresentation, such as in the cases of smoking status or past health issues, the insurer can deny your death claim. Alternatively, if they discover that you've been fraudulent while you are alive, they will void your policy and return any premiums paid. The only way to avoid this is to be honest with our life insurance agents and to fully disclose anything you feel may hinder you from obtaining insurance. If you have past or current health conditions that prevent you from qualifying for standard insurance, we do offer No Medical Life, Disability, and Critical Illness to ensure you don't have to go without.  #2 - The Insured Commits Suicide Within The First Two Years: All life insurance policies have a two-year exclusion period for deaths that occur as a result of suicide. This means that if you were to commit suicide within the first two years after the policy is issued or reinstated, the death benefit would not be paid.  #3 - Two Year Incontestability Period: For the first two years of a life insurance contract, the insurance company can re-evaluate its underwriting of the policy. If they discover that a material mistake (birthdate/smoking status/health information) was made in the application for coverage, the insurance company has the option of adjusting the premiums, adding exclusions, or voiding the policy. Thus, the policy is said to be contestable during the first two years. Reinstated policies are also contestable for the first two years following reinstatement. Once this contestability period has expired, the policy is said to be incontestable. This means that the insurance company cannot cancel the policy for any reason other than missed premiums, or fraudulent misrepresentation.  #4 - You Didn't Pay Your Premium:

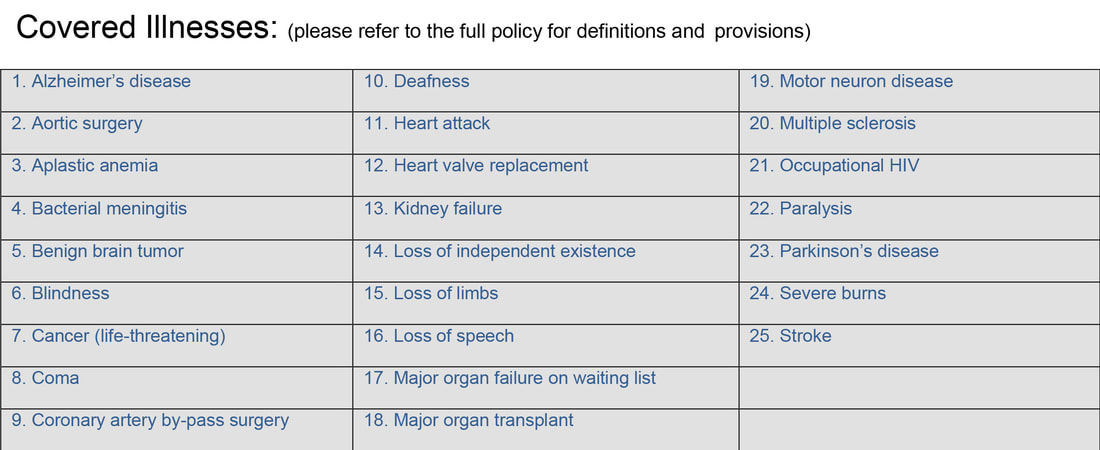

Missed premiums lead a policy to have a 30-day grace period where the premium must be paid for the policy to stay in force. If you fail to pay this premium after 30 days, the policy will lapse and need to be reinstated. Reinstatement may require proof of insurability, so it's best to ensure that your premiums are paid on time to avoid this hassle down the road. It's also noteworthy to mention that the incontestability period and suicide exclusion period will start again after reinstatement. Once you see that the reasons that a death claim can be declined are all valid and above board, you can put your fears and reservations about insurance to rest. Unlike a traditional mortgage insurance policy where they do most of their underwriting at claim time, our licensed insurance agents and up-front underwriting are your best bet. To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  Valentine’s Day is around the corner, and with so much focus on matters of the heart, let's talk about how to protect it! Your heart pumps blood to all of our organs, and throughout our body, it beats low when we sleep and high when we exercise, and above all, it keeps us alive. With heart disease being the second leading cause of death in Canada and 40,000 Canadians having sudden cardiac arrest every year, it's safe to assume that you know someone in your life who has been affected by one of these heart conditions. Critical Illness policies can provide a lump sum payout if you survive the waiting period (30 days) after suffering a critical condition or being diagnosed with a critical illness. For example, if you were to have a heart attack, and survived the attack, and waiting period, you would be eligible for a lump-sum payment of whatever your policy was. Coverage is available from $25,000 to $1,000,000 and covers 25 conditions, including life-threatening cancer, kidney failure, multiple sclerosis, and strokes.  If you've had a history of health conditions, you may think you will not qualify for Critical Illness insurance. However, at Broker Plus Insurance, we like to leave no stone unturned, so we have a No Medical Critical Illness product that can be placed for clients who may not qualify for our standard Critical Illness insurance. Clients can insure $5,000 to a maximum of $300,000 on this type of policy. Strokes, cancer and coronary surgery are covered under our No Medical Critical Illness policy.

Don't forget about the kids too! We have a Child Critical Illness Rider and a standalone Child Critical Illness policy to ensure the entire family is covered! To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  We are starting the year off right with new lower rates for personal life insurance policies! We know it’s not in every client’s budget to include mortgage protection, and that’s a shame. These reduced rates will make it more affordable for you and your family to obtain coverage or even partial coverage. Coupled with the fact that personal life insurance is a cheaper alternative to traditional mortgage insurance, we’ve got the best options for your insurance needs! These life policies are also entirely customizable, allowing you to control more aspects of your insurance policy.

Additional Benefits:

Coverage Enhancements:

A lot of clients, like mortgage brokers, can get frustrated and confused by the insurance options and advice that they may be getting from friends, family, and, of course – the lenders. The best thing you can do is to contact our company for a free no-obligation quote, to ensure that your insurance needs are being met with the best products and rates possible. Start off 2020 with less stress, by utilizing Broker Plus Insurance, we’ve got your insurance needs covered! To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  It’s the most wonderful time of the year unless you have the mindsets of Ebenezer Scrooge or The Grinch before they had their Christmas epiphanies. However, for many of us, Christmas is a time where we get together with family and friends, celebrate the season, and to spread comfort and joy. While you’re enjoying a glass of eggnog, there are some things that are important to conspire by the fire; and these important things are insurance.

This year, we’re asking our clients to think outside the present box and educate themselves on just how important insurance is compared to that new plasma TV set they’ve wanted. Why is Insurance The Greatest Gift You Can Give?

Don’t let your insurance needs fall off Santa’s sleigh, contact us today for more information on how we can ensure you have a holly, jolly Christmas by ensuring their insurance needs are fully met. To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  We realize that not every client we come in contact with has the time for individual underwriting requirements such as paramedical exams. The benefit of our Canada Protection Plan (CPP) No Medical insurance products is that there is no medical exam required from the client! Recently, we were ecstatic to learn that CPP has raised its maximum amount of available coverage for their Express Elite Term Plans from $500,000 to $750,000! They have also relaxed the weight and height chart so that more clients can qualify for this product! Like all of our CPP products, the application is completed with a life agent and a questionnaire to keep this process simple and easy for your clients. However, we also realize that several of our clients will need specialty products due to a health history of serious medical conditions. This is where CPP has once again gone above and beyond by allowing clients with serious medical conditions who can apply for their A-Z Life Coverage; a product designed for the hard to insure! Coverage is available from $10,000 up to $500,000 without a medical. Riders For CPP Policies:

Additional Benefits Of CPP:

Free marketing materials for both products available here! The most significant accident you can make is thinking that with your health conditions, the online insurance you’ll qualify for Accidental Death insurance. Contact us today for more information on how these robust products can ensure your needs are genuinely protected! To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  Insurance can be equated to a horror movie to many of us, as we never know what’s lurking around the corner in the haunted house of life. While we hope to get out safely, we don’t know if Jason, Freddy or Pennywise is around the corner; waiting to catch us off guard. Unfortunately, what happens to many people, is they run through this haunted house frantically trying to evade the monsters who want to harm us. These monsters are cancer, death of a loved one, disability, and the worst, in my opinion – a critically ill child.

While running through the haunted house of life, frantically does work for some people, it’s not a practical solution to fighting off these monsters. No, you don’t need a knife, hatchet or chainsaw; what you need is insurance. Now imagine you’re trapped in this haunted house with another person named Georgie. Georgie confidently claims, “I have insurance through work, I’m covered three times my salary if I pass away; these monsters can’t hurt me!” Wrong Georgie, let’s break this down to make it a little easier to see why Pennywise grins from ear to ear when he hears someone say this. Georgie makes $50,000 a year if he passes away his spouse gets $150,000. While this amount is enough to cover three years without him; what about the other years he would have been alive? Does Georgie have children? If so, he will need much more than three years of coverage to ensure his family’s needs are taken care of. If Georgie was to take a Term 20 policy for $500,000; he would be able to have 10 years of his salary paid upon the time of his death, add the three years he gets paid from work – that’s 13 years of his lost salary wages his spouse will have to ensure his family can safely navigate through the haunted house of life without Georgie. Don’t fall into the pitfalls of work coverage as the magic potion for your needs; contact us today for more information. To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator.  It’s not a stretch to imagine that you’ve probably encountered many of your friends, coworkers, or family members who are worried about job stability in today’s changing economy. Regardless of what industry you work in, there seems to be a lingering threat that one day, you may be laid off of work. What’s more worrisome, is the thought of becoming disabled while having to support a family; especially if only one spouse is working.

With stress tests, mortgage payments, and life insurance, it’s easy to understand why many clients may not opt for an individual disability policy, particularly if they have group benefits available through work. However, with only 50%-70% of their pre-taxed income being covered under most group plans, there is another 50%-30% of funds that are unaccounted for and could be a detriment to someone who becomes disabled. In 2017, 6.2 million people in Canada had at least one disability, with a woman more likely to have a disability than men. Our Mortgage Disability coverage provides the reassurance that families need:

Possibly one of the best benefits of this policy is the optional rider for Job Loss insurance. According to Statistics Canada in January of this year, 88,000 jobs were lost and while many of these jobs were part-time; it isn’t hard to imagine the financial hardships some of these families faced while dealing with this loss. Job Loss must be taken at the time of purchase with the Mortgage Disability and has several benefits, including:

We have many marketing tools such as informative flyers, past client letters, and web buttons where your clients can request a quote for these products directly through your website! To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. *Statistics on Job Loss and Disability from https://www.cbc.ca/news/business/canada-employment-january-1.4527905 and https://www150.statcan.gc.ca/n1/pub/11-627-m/11-627-m2018035-eng.htm  If there’s one thing we dislike the most in our industry, it’s when a client is turned down for insurance. There’s a common misconception that if you’ve been turned down for coverage in the past, the only insurance you will qualify for is an Accidental Death mortgage insurance policy. This could not be further from the truth when you utilize Broker Plus Insurance for your mortgage and insurance needs. We can offer high-risk clients a FULL personal term insurance policy with our No Medical A-Z Life Coverage! Accidental Death policies will only pay out if you were to pass away as the result of an accident, leaving your family without any coverage on natural causes. As well, it is based on a declining balance and will only pay out the amount outstanding on a mortgage at the time of death. No Medical Life insurance is just like a standard Term Life policy with one exception; there’s no paramedical information required! You may be surprised to know that No Medical life insurance doesn't have to cost “an arm and a leg.” With 4 rate classes based on risk, we have access to the best custom no medical insurance in the market today! How Does No Medical A-Z Life Coverage Compare To Accidental Death?  As you can see, there are several benefits to looking at a No Medical policy compared to Accidental Death only. With the allowance of some pre-existing conditions, no paramedical exam and more robust coverage options; No Medical Insurance is definitely a better product to choose.

We are also excited to announce a new No Medical Express Elite product, which is suitable for relatively healthy clients. This product is perfect if your client leads a busy lifestyle, does not have time for a paramedical appointment, or perhaps they enjoy extreme sports such as skydiving that many insurance companies will not place a policy with. Whatever their reason is, we have the perfect product for your clients, which has a maximum of $500,000 coverage. To request a quote on the products we offer, click here. Or call: 1-877-242-8820 and press 3 to speak with an insurance coordinator. |

Author

All blog posts are written from Cassie Meadows, a Broker Account Manager at Broker Plus Insurance.

Archives

March 2021

Categories

All

|

RSS Feed

RSS Feed

|

|

|

|